- Artemis Big Fundamentals in Crypto

- Posts

- Maple Finance: The Hub for On-Chain Institutional Lending in Crypto

Maple Finance: The Hub for On-Chain Institutional Lending in Crypto

Alex Weseley

November 26, 2024

Overview

Maple Finance stands tall as one of the protocols that has managed to revolutionize institutional lending in the cryptocurrency space. Founded in 2019 and led by a team of former bankers and credit investment professionals, Maple aims to improve legacy financial markets. Maple has grown to become DeFi's Institutional Lender - providing yield on digital assets for capital allocators, while allowing borrowers to unlock liquidity against their assets to grow their business.

Maple Institutional is focused on providing overcollateralized loans to leading institutional borrowers with full underwriting and onboarding. The institutional focus has enabled Maple to scale and consistently deliver higher yields than its peers. The Maple platform allows Accredited Investors to participate and earn yield on their digital assets.

Syrup is Maple's DeFi native product, giving everyone permissionless access to the consistent high yield generated by Maple's institutional lending engine. Syrup is integrated with several of the largest DeFi platforms including EtherFi, Pendle and the OKX Web3 Ecosystem.

Maple Institutional and Syrup are united under the $SYRUP token, which governs the entire ecosystem. By staking $SYRUP, one can participate in the growth of Maple and earn staking rewards that come from the protocol treasury.

Here at Artemis, we emphasize delivering data-driven, unbiased reports designed to break down protocols in a way that’s accessible and easy to understand. Using a first-principles approach, we aim to showcase how Maple operates and highlight the fundamental metrics that set it apart, while also highlighting Maple’s upcoming launch, Syrup - an upgrade that entails a token swap and more. Let’s dive right in:

Breakdown: How Maple Works

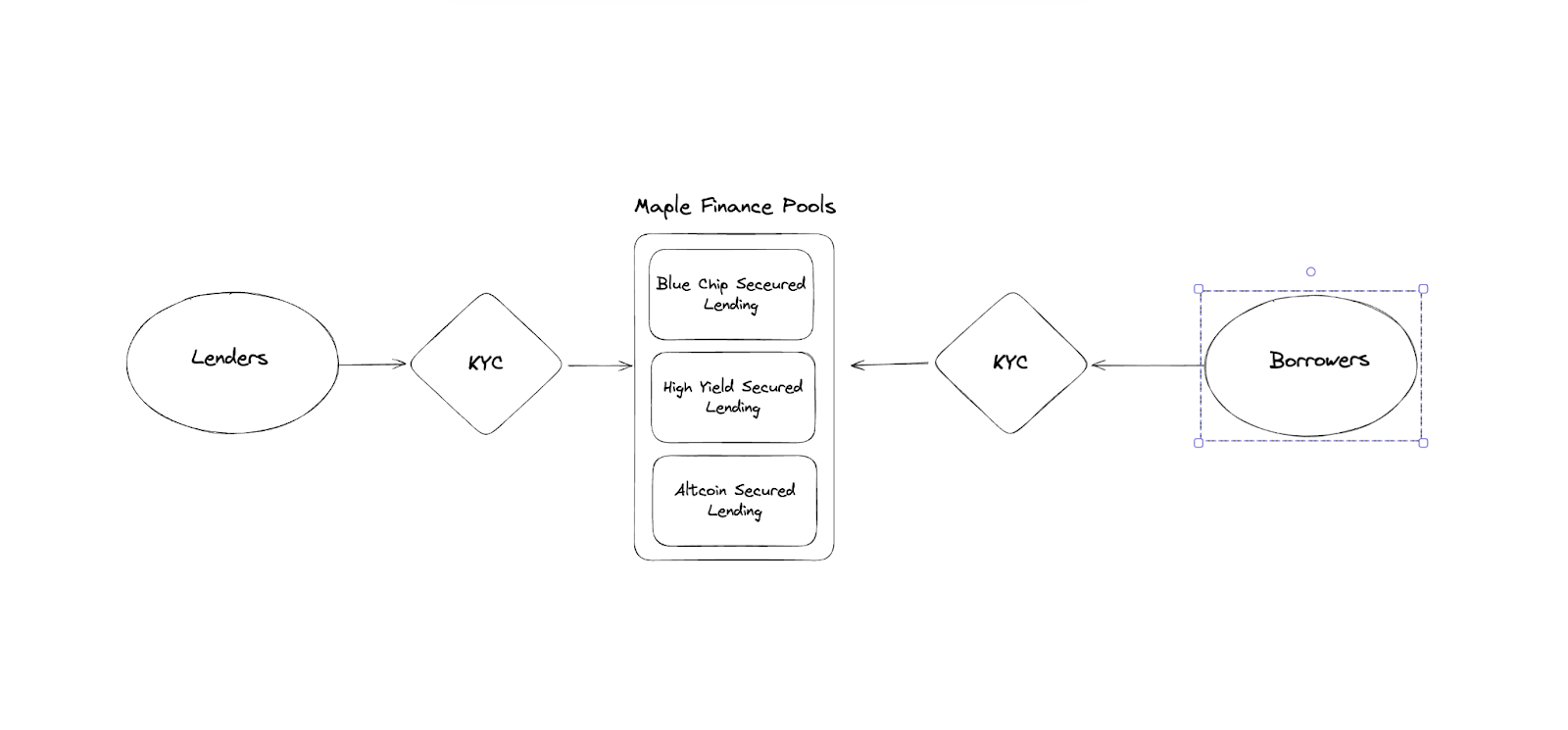

At its core, Maple is a permissioned, overcollateralized lending protocol that allows KYC’ed individuals or institutions to borrow and lend given certain conditions. Below is a diagram that simply illustrates how this works:

Fig 1. Maple Finance Diagram (Source: Artemis)

Maple Finance’s architecture comprises two core elements:

Pools

Borrowers & Lenders

Pools

Maple Finance offers multiple pools with different lending assets such as USDC and wETH. The pool strategies differ with some only being overcollateralized with BTC and ETH, while others allow different digital asset collateral types, such as SOL. Lenders who deposit into the pool will earn interest denominated in the pool’s lending asset, with the interest being determined by the loan terms set by Maple’s credit underwriting and risk management team.

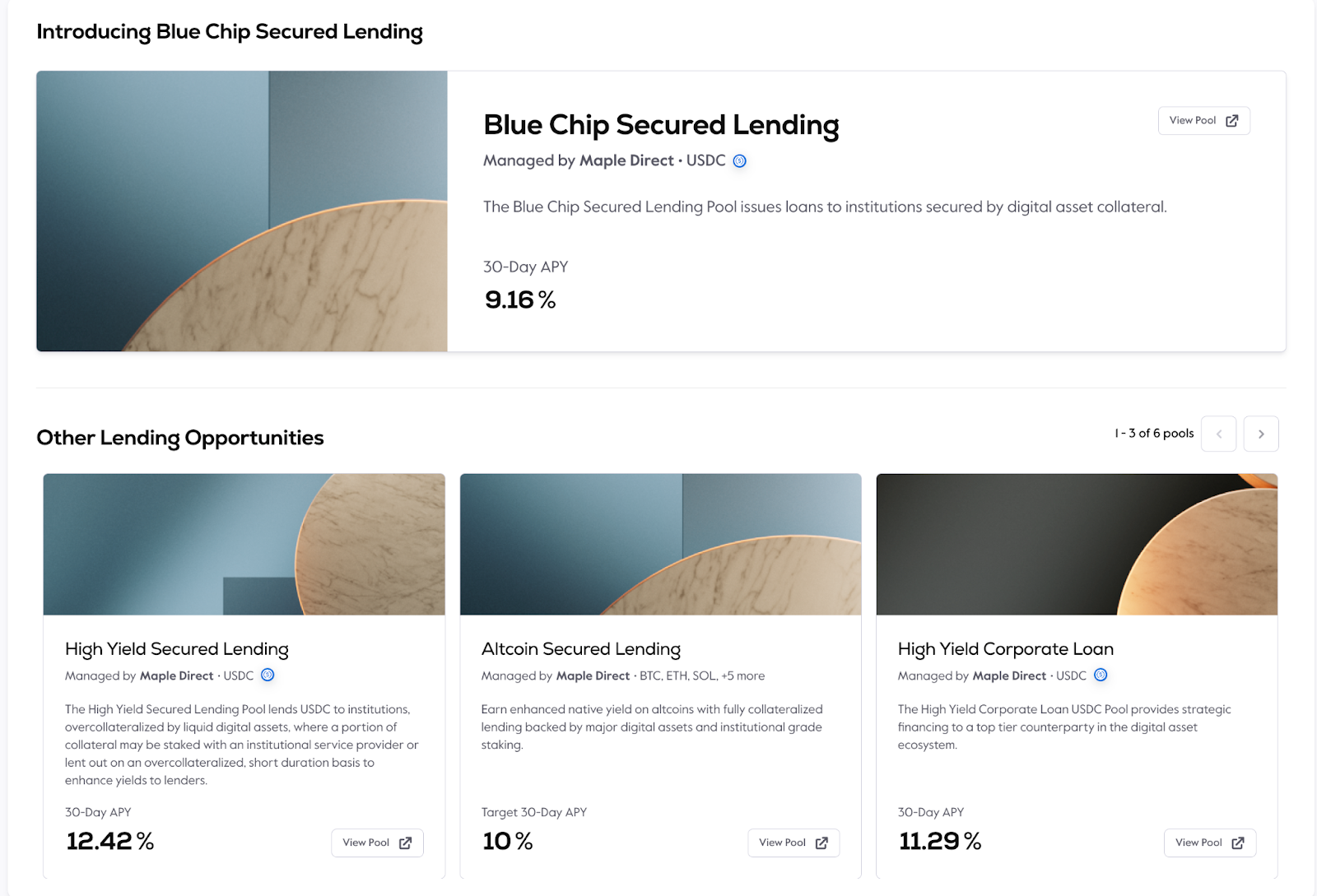

Below is an overview of some of the Maple pools currently available:

Fig 2. Maple Finance Pools (Source: Maple Finance)

In the Blue Chip Secured Lending Pool, for example, lenders deposit USDC, while borrowers provide BTC, SOL or staked versions of ETH as collateral with the collateral being held in qualified custody. . Maple has multiple pools, each pool with its own return, risk and liquidity profile to meet different lender and borrower needs.

The High Yield Secured Lending Pool accepts a broader range of digital assets as collateral, enabling lenders to earn higher interest rates, all generated with overcollateralized lending.

These different pool structures allows for diversification of risk and enables Maple to offer various lending options to meet different liquidity, risk, and return requirements for both lenders and borrowers in the space.

Borrowers & Lenders

Maple Finance is set apart from other permissionless lending platforms because they perform Know-Your-Customer (KYC) checks on all lenders and borrowers across the platform, which include:

The collection of documentation and information to identify the user. In case of an Entity, the Ultimate Beneficial Owners and Directors are identified as well.

Accreditation checks on Lenders

PEP and Sanction scans for all users.

Scanning lender wallets before deposit for risk factors using TRM Labs. Lender wallets that hit on risks (including interaction with high risk counterparty wallets) are blocked.

Maple’s Incredible Growth

500% Increase in Total Value Locked

Today, Maple is a behemoth in the lending sector, having grown an incredible amount in the past few quarters. Maple Finance has demonstrated remarkable growth, driven by its focus on compliance, security and transparency. With over $5 billion in loan originations, Maple has positioned itself as a leading provider of high-quality on-chain credit solutions.

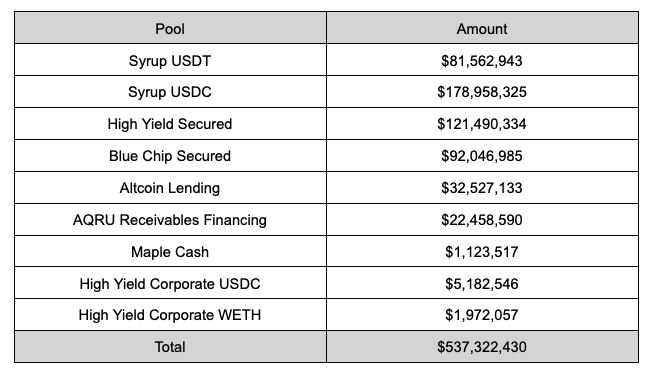

Fig 3. Maple Finance TVL (Source: Artemis Maple Dashboard)

Maple’s TVL has shown incredible growth over the past year, with over 500% in TVL growth in 2024 alone. Maple continued to scale all throughout the summer of 2024, while asset prices were ranging for months - indicating that institutions and DeFi natives were actively seeking yield on their assets and utilizing Maple Finance. It underscores the confidence both lenders and borrowers have in Maple’s approach to secure and accessible credit solutions.

With the recent expansion of pools such as Syrup USDT and Syrup USDC having already reached a combined $260m of TVL already, it reflects Maple’s ability to attract both conservative and high-yield-seeking lenders.

By offering a variety of risk profiles, Maple enables a tailored approach to DeFi lending that appeals to a wide audience, from blue chip overcollateralized lending, to higher-yield altcoin lending. Overall, the consistent and exponential nature of the TVL growth showcases the accelerating demand for Maple’s products.

Revenue increasing 230% Quarter Over Quarter To 930K

Maple’s revenue comes mainly from three different sources:

Origination Fees (fixed-term only): Fees paid by borrowers during loan funding and refinance operations, deducted from their drawable balance of principal.

Service Fees: Fees paid by borrowers during loan payments, added to gross interest.

Management Fees: Fees taken as a portion of gross interest paid by Borrowers when payments are made.

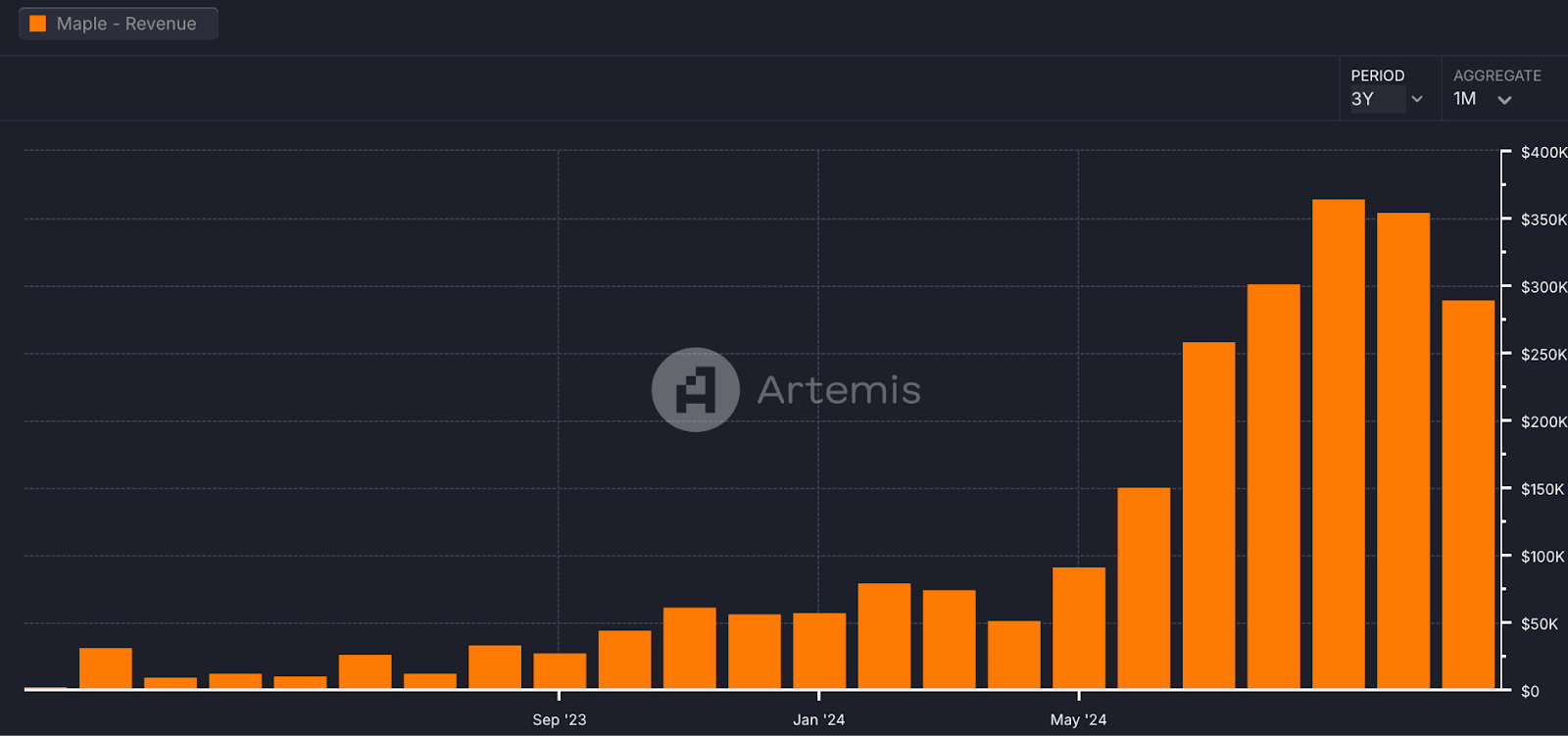

Fig 4. Maple Finance’s Monthly Revenue (Source: Artemis Maple Dashboard)

As we can see, Maple’s revenue has increased quarter over quarter sustainably over the past year. This is a natural outcome of increased TVL, as it means that more users are utilizing the platform - a great sign of growth in the business side. Maple as a protocol shows no sign of slowing down - with increasing revenue, this allows Maple to continue scaling institutional lenders, and capture more demand.

Fig 5 shows that while Maple is still Net Loss, their Revenue has increased tremendously Quarter-over-Quarter, with more than 1000% growth from Q3 2023 to Q3 2024. In a DeFi space where many 2021-2022 projects have faded away due to unsustainable models or regulatory pressure, Maple’s resilience stands out as a key differentiator.

By maintaining a strong focus on compliance, transparency, and quality partnerships, Maple has positioned itself not only to survive but to thrive. This resilience and growth underscore Maple’s potential to achieve profitability as it continues to expand its pool offerings and refine its lending solutions, setting a high bar for sustainable growth in the DeFi lending space.

Fig 5. Maple DAO Revenue & Expenses (Source: Q3 Treasury Report)

Lastly, a look at loan numbers - it’s again, clear to see that Maple has found product-market fit, with total active liquidity of the protocol up 3x over the year, and total loan originated up 30% in the year.

Fig 6. Maple Finance Liquidity & Loan Numbers (Source: Q3 Treasury Report)

Competitive Landscape

Amongst Traditional De-Fi Protocols

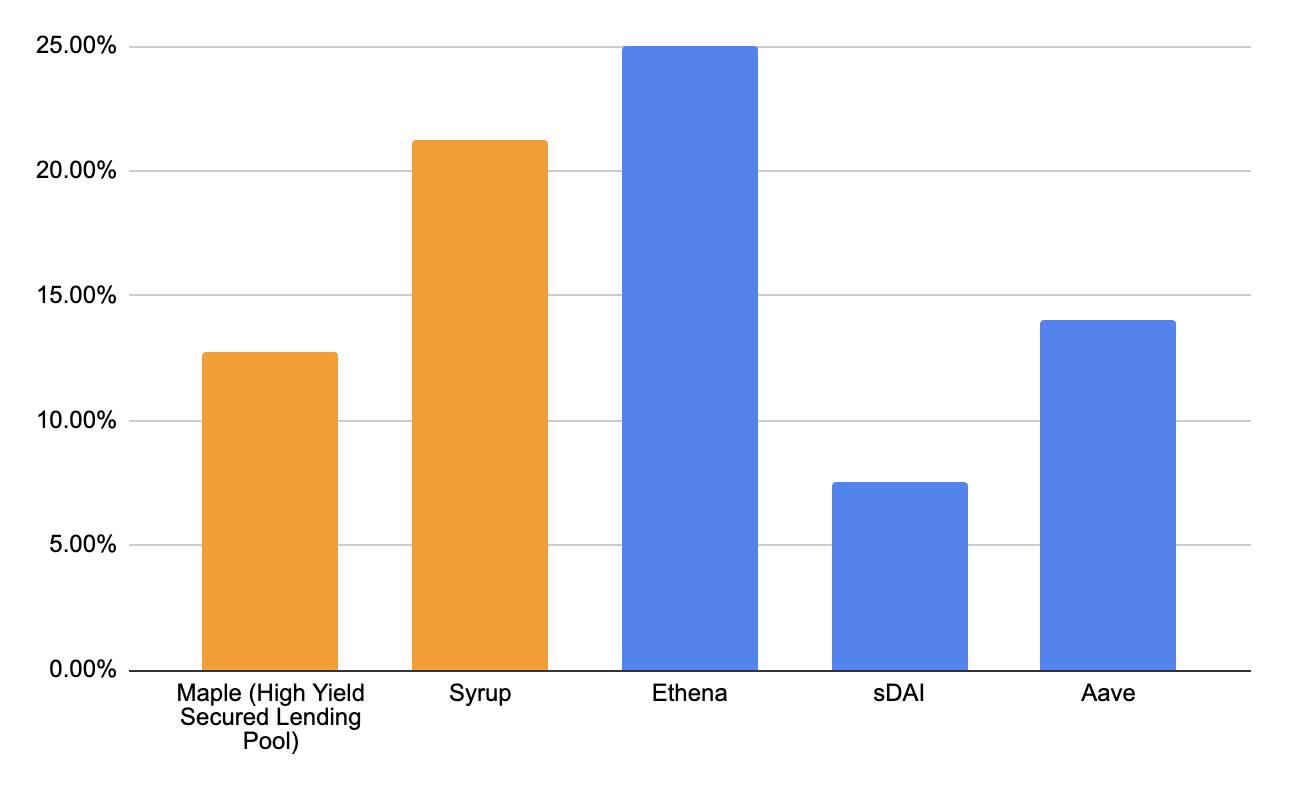

Maple has become the preferred destination for corporate treasuries and native DeFi yield funds - and we can see why. Maple offers better USDC rates for lenders across all traditional DeFi platforms, currently sitting at 17.7% for Maple and 12.44% for Syrup.

Fig 6. Latest DeFi USDC Yields As Of 25 November (Source: Artemis)

This indicates that borrowers are willing to pay higher interest rates for the peace of mind that comes with Maple’s structured, fully collateralized lending pools and rigorous risk management. On top of that, Maple defines their relative targets, so that their risk management strategies can withstand different market conditions. Their Blue Chip Secured pool targets yields ~4-5% higher than variable rate DeFi lending protocols (like Aave or Morpho), whereas their High Yield Secured pool targets ~5-7% above Blue Chip Secured, and Syrup, as a hybrid of the two strategies, will sit in between the two.

Secondly, Maple has clever duration management strategies - when there is lower borrower demand and market rates fall, they issue shorter term loans. This means they can enforce borrower repayment within 7-14 days, setting up flexibility to re-issue loans at higher rates when market conditions change.

Shorter tenor loans also improve liquidity in a time when withdrawal needs are naturally more elevated than average. When the market is ‘hot’ and rates across DeFi are elevated, the Maple team shifts tact to thinking about sustainability and long term outperformance. They begin issuing loans with longer time frames to lock in the higher yield environment.

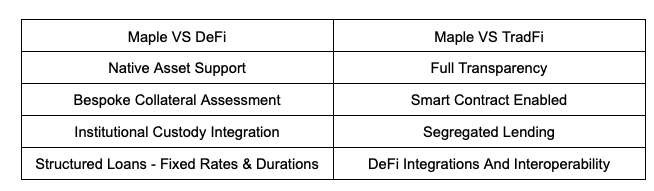

Generally, Maple has a strong argument against DeFi and CeFi - as seen in Figure 7, Maple offers a lot more flexibility than CeFi, and more structure than DeFi - bridging the best of both worlds together.

Fig 7. Maple vs DeFi and Maple vs TradFi (Source: Artemis)

Amongst RWA Protocols

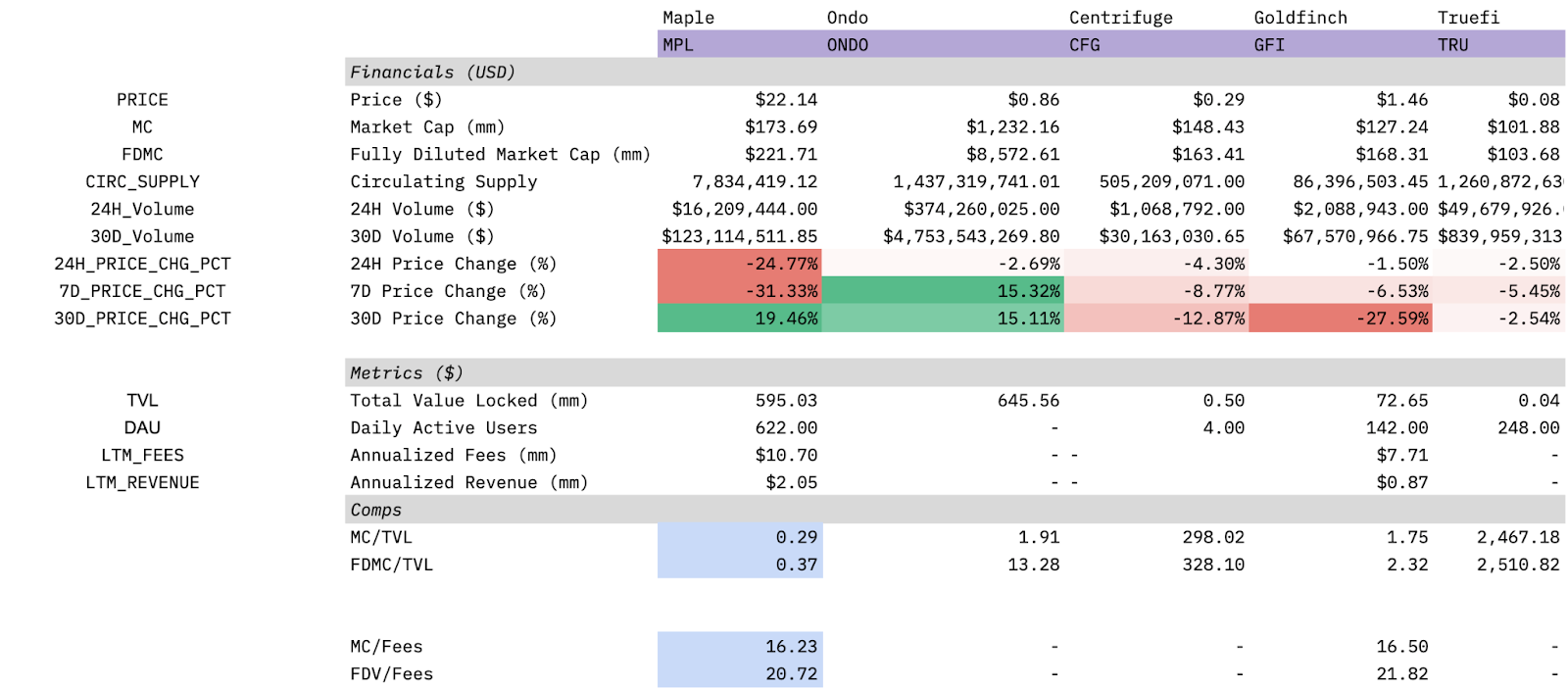

Maple Finance operates in a competitive niche that includes protocols like Goldfinch, TrueFi, and Centrifuge. Each platform offers a distinct take on lending. Here’s how Maple stacks up:

Fig 8. Maple vs RWA Protocols (Source: Artemis)

Maple exceeds the other protocols by miles, with a dominant position in total value locked (TVL) on its platform. In the crypto space, no other Real World Asset (RWA) protocol comes close to Maple in terms of lending volume, which naturally translates to the highest revenue among all RWA platforms.

A large reason for this is that RWA lending is relatively new, and Maple has an incredible first-mover advantage amongst the other on-chain protocols that do similar strategies. It’s worth noting that if compared to traditional De-Fi protocols such as Aave and Maker, Maple would reflect lesser TVLs and lower metrics - however, Maple is first and foremost an institutional borrow-lending protocol, and a De-Fi protocol second. As such, Maple dominates in that singular category amongst other protocols, and continues paving the way for on-chain TradFi.

Maple & Syrup

What is Syrup

Syrup is Maple’s newest launch - powered by Maple, Syrup provides institutional yield to the wider DeFi ecosystem. Syrup combines the strength and security of Maple's renowned lending infrastructure with the flexibility and inclusivity of DeFi, and derives the yield from a blend of Maple High Yield Secured and Blue Chip Secured lending pools. Syrup enables partnership with broader DeFi that otherwise wouldn’t be accessible through Maple, such as having wallet partnerships with OKX & Binance wallets, allowing users to earn additional rewards.

Syrup leverages the same smart contract infrastructure and borrower network as Maple, but offers permissionless access through DeFi. While Syrup has direct access to Maple pools through its interface, Maple establishes new unique pools for Syrup to ensure that proceeds and risks are segmented from existing pools accessible to Maple customers.

It’s also worth mentioning that lending is permissionless on Syrup - instead of needing KYC, users can simply connect their wallet, deposit funds, and earn the yield.

The Growth Of Syrup

Despite just launching in late Q2 2024, Syrup scaled extremely quickly to 280M in TVL. Syrup USDT eclipsed Syrup USDC as the fastest growing product in Maple’s history, crossing 45M in TVL by month end.

It’s also worth noting the partnerships Syrup has managed to capture:

Fig 9. Syrup Stats

Syrup Token

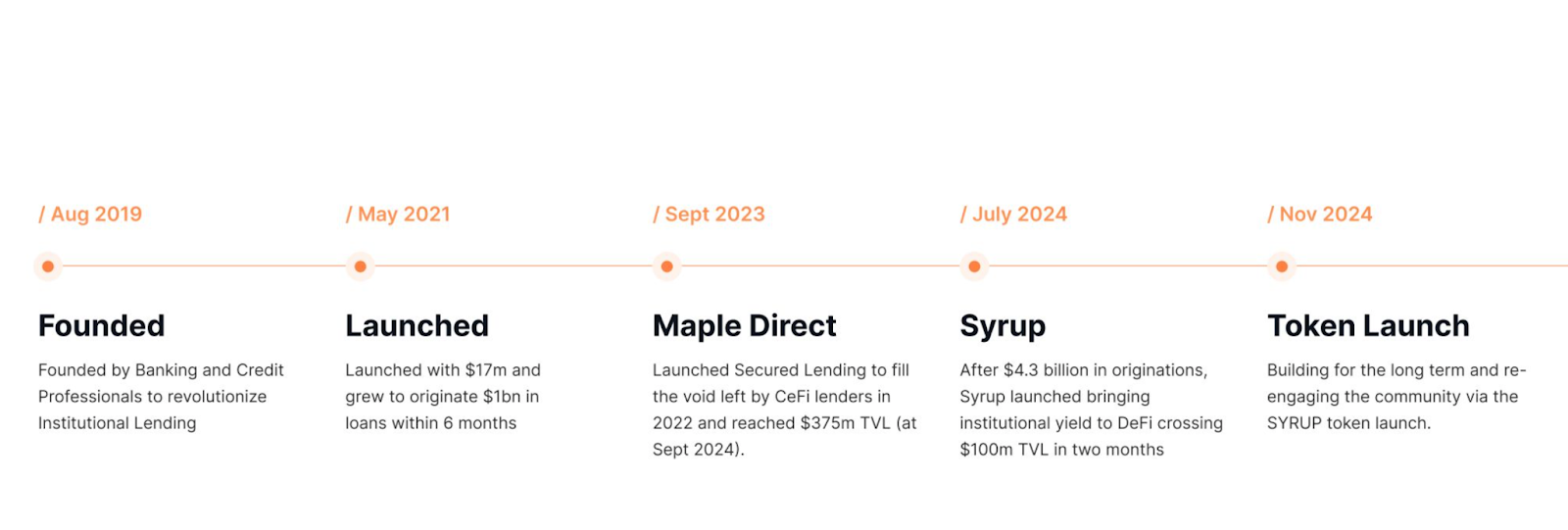

Lastly - in the MIP-010 proposal, a Syrup token was proposed, and MPL would be converted to Syrup. The Maple team has executed on this, with Syrup having been launched on November 13th, 2024, and existing MPL holders being allowed to convert their MPL for Syrup at the rate of 1 MPL = 100 SYRUP.

Fig 10. Roadmap

The token does have utility - Fee revenues generated from Maple’s and Syrup’s lending operations can be used to buy back the SYRUP token, which will form part of the token emissions that go to stakers. Below we’ve outlined what Syrup token holders can expect -

$SYRUP Token holders:

Are Part of DeFi’s Institutional Lender – Supporting the leading platform driving institutional credit within DeFi.

Can Stake SYRUP for Rewards – Align with Maple’s growth and earn sustainable rewards through staking.

Shape the Future – Participate in governance by voting on key decisions, including staking rewards and protocol enhancements.

Concluding Thoughts

Maple Finance has emerged as a pioneer in overcollateralized lending within the DeFi ecosystem, positioning itself at the intersection of decentralized and traditional finance. With the launch of Syrup that captures the DeFi ecosystem and the existence of Maple that captures the more institutional borrowing and lending - Maple is poised to tap into both retail and institutional capital.

As the crypto market evolves towards a more structured and professional landscape, institutions will increasingly look to protocols like Maple as a trusted platform for institutional-grade lending solutions. Maple's commitment to compliance, transparency, and risk management aligns with the requirements of institutional investors, setting it apart as a reliable partner for corporations and asset managers exploring the DeFi space.

For asset managers and institutional investors, understanding Maple’s evolving framework is crucial to navigating DeFi’s next wave of innovation. Maple’s 2030 vision is to eventually become the largest facilitator of on-chain credit worldwide. At the rate Maple is growing, the platform has a clear path to achieving this ambitious goal.